5 Simple Habits That Help You Stay on Budget Every Month

- David E. White

- Aug 4, 2025

- 4 min read

Updated: Mar 25

If you want to stay on budget every month, the key is not perfection. It is simple habits done consistently.

Most people struggle with budgeting, not because they lack income, but because they lack a clear system.

The good news is this:

Simple habits, applied consistently, can help you stay on budget every month and take control of your money with confidence.

What You Will Learn

• How to stay on budget every month without stress

• A simple system to control spending

• How to build habits that actually stick

• A proven budgeting method you can start today

1. Start with a Written Budget

Writing things down makes your money plan real.

Use pen and paper or a simple spreadsheet. Start each month with a clear plan for:

• Income

• Bills

• Savings

• Spending

Even if you fall off track, a written plan helps you reset quickly.

Tip:

Keep it simple. The best budget is the one you will actually use.

2. Track Every Dollar Spent

You cannot stay on budget every month if you do not know where your money is going.

Track your spending for 30 days. You may be surprised how quickly small purchases add up.

Simple tool:

Your smartphone plus a notebook or planner.

This is one of the easiest and most powerful habits you can build.

3. Automate What You Can

Make your system work for you.

Set up:

• Auto-pay for bills

• Auto-transfer for savings

This helps you stay ahead and removes the temptation to spend first.

Think of it as:

Set it up once. Benefit every month.

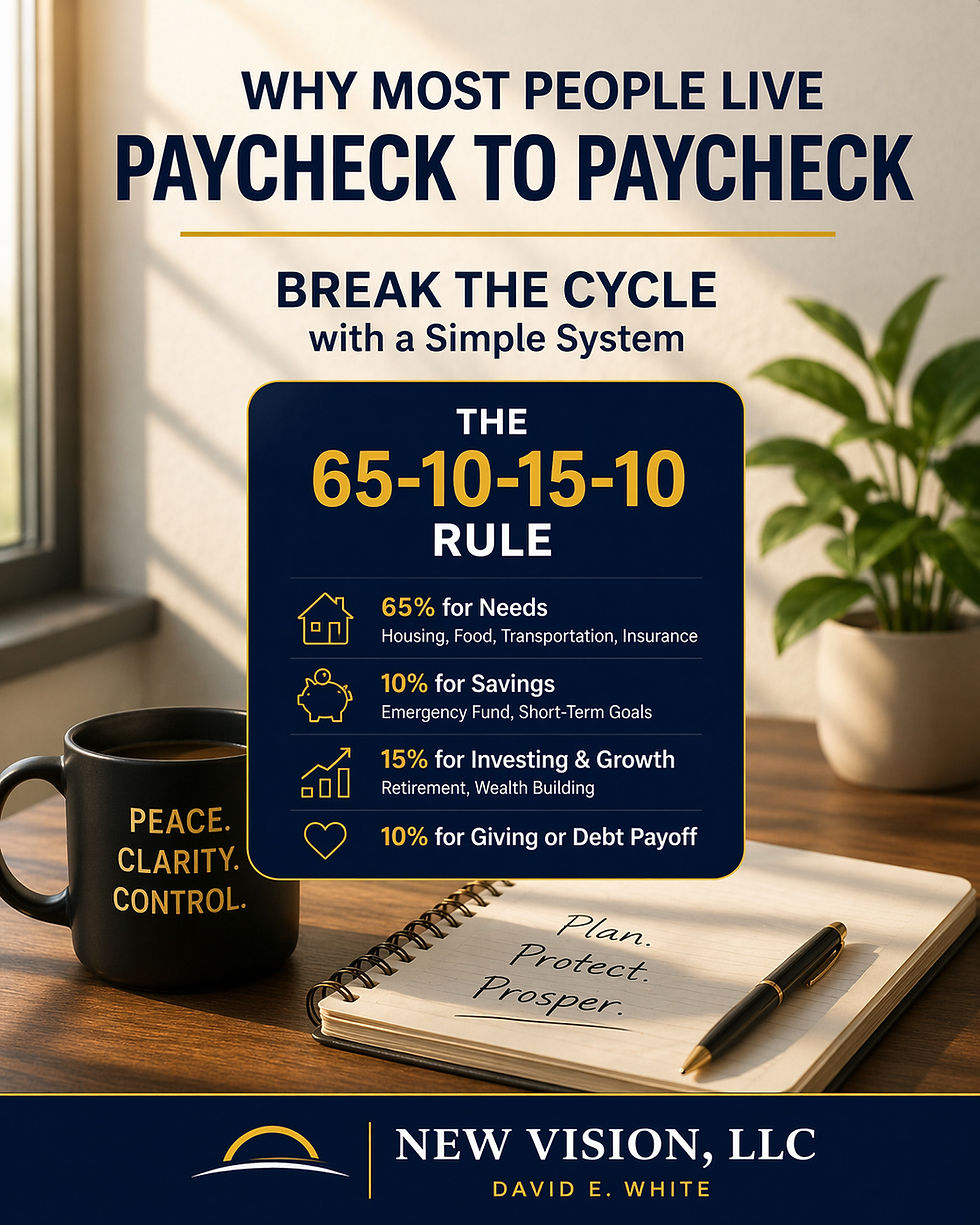

4. Use the 65-10-15-10 Rule

This system helps you stay on budget every month by giving every dollar a purpose:

• 65% Needs

• 10% Savings

• 15% Investing

• 10% Giving or Debt Payoff

Example:

Take-home income: $30,000.00 per year ($2,500.00 per month)

Needs:

$30,000.00 × 65% = $19,500.00 per year

$19,500.00 ÷ 12 = $1,625.00 per month

Savings:

$30,000.00 × 10% = $3,000.00 per year

$3,000.00 ÷ 12 = $250.00 per month

Investing:

$30,000.00 × 15% = $4,500.00 per year

$4,500.00 ÷ 12 = $375.00 per month

Giving or Debt Payoff:

$30,000.00 × 10% = $3,000.00 per year

$3,000.00 ÷ 12 = $250.00 per month

Take-home income: $60,000.00 per year ($5,000.00 per month)

Needs:

$60,000.00 × 65% = $39,000.00 per year

$39,000.00 ÷ 12 = $3,250.00 per month

Savings:

$60,000.00 × 10% = $6,000.00 per year

$6,000.00 ÷ 12 = $500.00 per month

Investing:

$60,000.00 × 15% = $9,000.00 per year

$9,000.00 ÷ 12 = $750.00 per month

Giving or Debt Payoff:

$60,000.00 × 10% = $6,000.00 per year

$6,000.00 ÷ 12 = $500.00 per month

Take-home income: $100,000.00 per year ($8,333.00 per month)

Needs:

$100,000.00 × 65% = $65,000.00 per year

$65,000.00 ÷ 12 = $5,417.00 per month

Savings:

$100,000.00 × 10% = $10,000.00 per year

$10,000.00 ÷ 12 = $833.00 per month

Investing:

$100,000.00 × 15% = $15,000.00 per year

$15,000.00 ÷ 12 = $1,250.00 per month

Giving or Debt Payoff:

$100,000.00 × 10% = $10,000.00 per year

$10,000.00 ÷ 12 = $833.00 per month

This system helps you stay on budget every month by giving every dollar a job and a clear purpose.

5. Review Weekly, Not Monthly

Most people wait until the end of the month to realize they overspent.

Instead:

Review your spending every 7 days.

This allows you to make small corrections and stay on budget every month with confidence.

----------

Ready to take the next step?

Start here:

Budgeting & Saving Matter More Than Ever - Why Budgeting and Saving Are Important

Step 1: Read

Understand the foundations of budgeting and why they matter.

Step 2: Learn

HOW TO BUDGET & SAVE

UNLOCK FINANCIAL FREEDOM: SIMPLE BUDGETING STRATEGIES FOR EVERY INCOME LEVEL

Step 3: Apply

Create your written budget and begin tracking every dollar this week.

Step 4: Plan for the Future

Use the Retirement Burn Rate Calculator Kit to understand how long your money can last and make better long-term financial decisions.

Affiliate Disclosure

This post contains affiliate links. If you make a purchase, I may earn a small commission at no extra cost to you.

Continue Learning

Next:

How to Save Money Even If You’re Living Paycheck to Paycheck

Website

Peace. Clarity. Control.

Disclaimer

The information provided in this blog is for educational and informational purposes only and reflects the personal opinions and experiences of the author. It should not be considered financial advice. Always consult with a licensed financial advisor before making any financial decisions.

David E. White

Author | Blogger | Financial Educator

Over 20 Years of Business Ownership Experience

NEW Vision, LLC

Comments